If a taxpayer’s GST registration is canceled, the taxpayer is no longer required to pay or collect GST, becomes ineligible to claim the input tax credit and do GST Return Filing. Section 29 of the CGST Act, together with Rules 20–22 of the CGST Rules, govern the cancellation of a GST registration. This article discusses important information regarding cancellation of GST Registration by tax officers.

Cancellation of GST Registration using Form GST REG-17

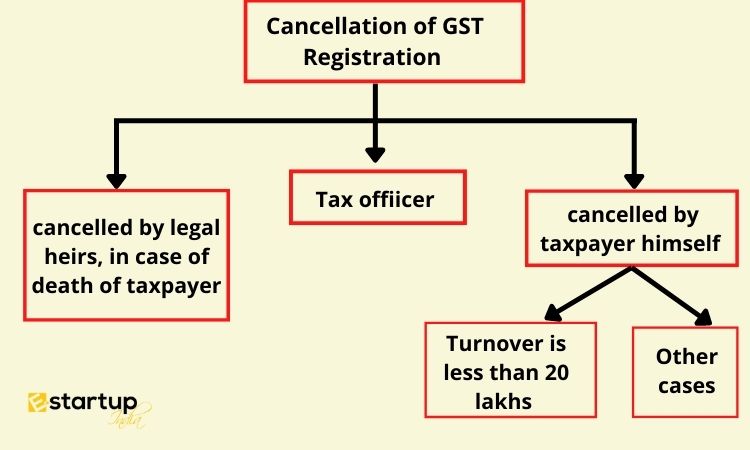

A taxpayer and an appropriate officer have the authority to request the cancellation of a GST registration. A show-cause notice in GST REG-17 form is issued by the appropriate official to trigger GST cancellation procedures.

Reasons for which Procedure for Cancellation of GST Registration by Tax Officer Occurs

- If a taxpayer who is part of the composition scheme under GST fails to submit GST tax returns for three consecutive years, the tax officer will cancel their GST Registration.

- For six consecutive periods, a taxpayer (other than a composition taxpayer) fails to file tax returns.

- The assessee voluntarily registered for GST but has not begun conducting business within the allotted time frame.

- The taxpayer has violated the GST Act or the rules enacted to implement the Act.

- With deceit or a deliberate misrepresentation, the GST registration is acquired.

- To avoid paying tax or getting a refund by wrongly using the input tax credit, a taxpayer may provide products or services without issuing an invoice or produce an invoice without having provided the goods or services.

- When a taxpayer misses the GST department’s three-month payment deadline for tax, interest, or penalties.

- Cessation of operations for the taxpayer.

- One-person company goes out of business due to the owner’s death.

- The taxpayer’s constitution changed, necessitating a new PAN.

- The affected individual is exempt from GST registration and has no further tax obligations.

- Corporate transition as a result of amalgamation or merger.

Important details to mention in the Form GST Reg-17 for tax officer

- Provide a detailed justification for why you think GST registration should be canceled.

- Notify the taxpayer that response in GST REG-17 must be submitted within seven business days after the date of notice.

- There must be a personal hearing if one is necessary, and the date and time of the hearing must be specified.

Procedure of Cancellation of GST Registration by a tax officer

If the appropriate officer is satisfied with the response, he may dismiss the case and issue an order using GST REG-20. If he is unsatisfied, he may revoke the taxpayer’s GST registration by issuing a Form GST REG-19 Cancellation Order. To appeal against cancellation of GST registration in India, you need to follow a procedure. The procedure is known as Revocation of cancellation of GST registration.

What is the GST REG-20 Form for Order dropping Registration cancellation?

If the taxpayer provides a response on Form GST REG-18, the appropriate officer will review it. If he is pleased with the response, he can dismiss the proceedings by making an order using GST REG-20. In addition, the authorized officer may dismiss the proceedings and issue an order in Form GST REG-20 if the taxpayer does not respond to the notification but subsequently files all outstanding returns and pays all such taxes, interest, and late fees due.

moreover, If you want any other guidance relating to GST Return Filing or GST Registration, please feel free to talk to our business advisors at 8881-069-069.

Download E-Startup Mobile App and Never miss the latest updates narrating to your business.