GST is an indirect taxation system in India. It applies to many exporters and importers. To increase the exports of India and boost the Indian economy, the government provides GST Registration for zero rated supplies. Many people confuse zero rated supplies with Non-Taxable Supplies or exempt supplies. Therefore, In this article, you will get a clear understanding of GST Registration for zero rated supplies.

What is GST?

GST stands for Goods and Services Tax. It is the current indirect taxation system that has replaced many previous indirect taxes. Furthermore, It is a destination-based tax, and the government levies it on the supply of goods and services.

It is an indirect tax applicable for the whole country. Under the GST Regime, the government levies the SGST, CGST, and IGST, and the difference between these three is as follows.

| IGST | CGST | SGST |

| Applied on the inter-state supplies of goods and services | Levied on the Intra-State Supply of both goods and services by the Central Government | Levied on the Intra-State supply of both the goods and services by the State Government |

| Tax sharing between Central and the State government | In CGST, Tax goes to the Central Government | The tax goes to the State Government |

What is GST Registration?

GST Registration is mandatory registration that every business whether supplying goods or services has to get if the annual turnover exceeds Rs. 40 Lakhs. (Rs. 20 Lakhs for Eastern or the Special States.) However, GST Registration in India is also mandatory for some businesses such as e-commerce businesses. It is also mandatory for Casual Taxable Persons and Non-Residential Taxable persons in India. To know more about GST Registration, you can use our guide GST registration.pdf or contact our GST experts at – 8881-069-069.

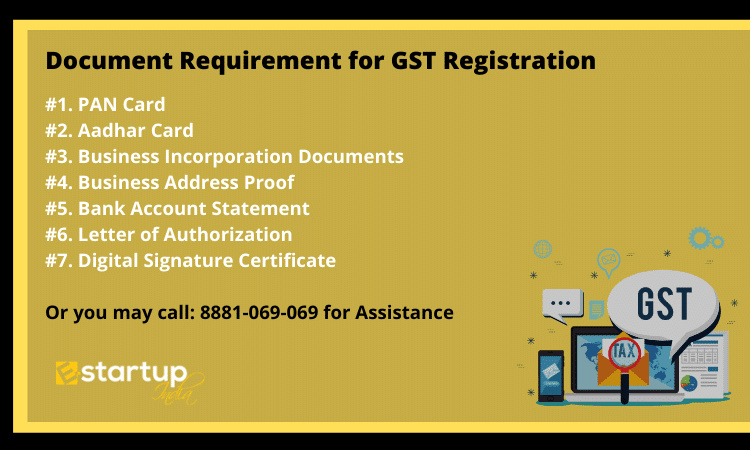

The Document Requirement for GST Registration in India is as follows:

What is Zero Rated Supply?

In India, there is no GST on exports. As a result, all export supplies GST-registered taxpayer makes zero-rated. A zero-rated supply, according to Section 16 of the IGST Act, is any of the following items or services:

- Export of commodities, services, or a combination of the two;

- Providing of commodities, services, or both to a developer of a Special Economic Zone

- Supplying a Special Economic Zone unit with products or services, or both.

What is GST Registration for Zero Rated Supply?

GST Registration for Zero Rated Supply is mandatory. Thus, it allows you to claim input tax credit refunds. One can claim refunds under GST Registration for Zero Rated Supply through:

- The dealer can either export under a bond or a LUT (Letter of Undertaking) and seek reimbursement of the tax input credit; or

- The dealer can pay IGST while making supply and then claim a refund.

As a result, the dealers have the freedom to pick between any two solutions that suit their needs.

Procedures for Refunding Goods Exported

The procedure of requesting a refund under GST legislation has been simplified for export dealers. Also, there is no need to file a separate refund application (GST RFD-01) for Zero-Rated Supplies. So, the procedure for getting refunds on taxes for exported goods is as follows:

- An export manifest must be filed by the person transporting the items; and

- The applicant should be doing GST Return Filing of the GSTR-3 or GSTR-3B returns correctly.

Procedures for Refunds on Services and Supplies Exported to a Special Economic Zone

The Refunds on Services and Supplies exported to a Special Economic Zone are available. In this scenario, you must make a refund claim using Form GST RFD-01. The following documents must be submitted with the reimbursement claim by service exporters:

- A statement listing the number of invoices and their dates; and

- Certificates of Bank Realization / Certificates of Foreign Inward Remittance

Along with the reimbursement claim, the provider of products or services to an SEZ must file the following:

- A statement listing the number of invoices and their dates; and

- Proof of receipt of goods or services that has been authorized by an SEZ official.

- Payment information

- A statement indicating the SEZ(Special Economic Zone) or its developer has not claimed an input tax credit for taxes paid by the supplier.

Provisional Refund of GST Registration for Zero Rated Supplies

On a preliminary basis, SEZ exporters and suppliers are entitled to a 90 percent reimbursement. Consequently, Within seven (7) days of receiving the rebate claim, a provisional reimbursement is issued. The claimant’s bank amount will be credited with the amount of the provisional reimbursement. However, Provisional reimbursements are subject to a condition. If the applicant has been penalized for any violation under the GST legislation or an earlier statute during the last five (5) years, the provisional refund will be denied. In addition, The amount of tax avoided in such a case must be greater than Rupees 250 lakhs (Rs. 2.5 Crores).

Moreover, If you want any other guidance relating to GST Registration, please feel free to talk to our business advisors at 8881-069-069.

Download E-Startup Mobile App and Never miss the latest updates narrating to your business.